Who Should Use a 3-Account Budget?

- Melissa Fidler

- Apr 8

- 4 min read

Not every budgeting method is built for every person. A system that works for a single person with no fixed expenses looks completely different from one that works for a woman with bills, a family, and a paycheck that never seems to stretch far enough.

The 3-account budget system is not a universal prescription. But for certain people, in certain situations, it is the exact structure they have been missing.

Here is a clear-eyed look at who this system works best for. And who might need a different approach.

This System Is Built for You If...

Your money disappears after payday

You get paid, you pay a few things, and somehow it is gone. Not on anything big. Not on anything you can clearly point to. It just vanishes.

This usually happens when money sits in one account with no separation. It blends together and disappears. The 3-account system gives every dollar a destination the moment your paycheck lands, so payday stops feeling like a countdown to broke.

You are living paycheck to paycheck (Even with decent income)

You're making it to the next payday but just barely, with nothing left over and nothing saved. Living paycheck to paycheck is rarely a math problem. When your bill money and your spending money live in the same account, there is no real boundary between them.

This is the exact situation The Breakthrough Flow™ was built to solve. The 3-account system creates that boundary automatically.

You hate tracking every dollar

If logging every transaction, categorizing every purchase, and reviewing your spending report every week sounds like a part-time job you never signed up for, you are not alone. Most people who try tracking-based budgets abandon them within a month. They quickly find the method requires more daily effort than real life allows.

The 3-account budget replaces tracking with structure. The Breakthrough Flow™ is designed as a one-time setup that runs in the background instead of something you redo every month.

This system does not ask you to track anything. Your Spending Account balance is your tracker. When it reaches zero, you stop. That is it.

Budgeting feels overwhelming

Have you

tried to budget before and felt immediately overwhelmed by the rules, the categories, or the sheer number of decisions required? The 3-account system was designed as the antidote to that feeling.

It simplifies your entire financial life into three questions: Are my bills covered? What can I spend today? Is my savings growing? When you can answer all three with a quick glance at your bank app, overwhelm goes away.

This System Might Not Be for You If...

You love tracking expenses

If reviewing your spending by category genuinely excites you. If you enjoy knowing exactly how much you spent on dining, clothing, and subscriptions each month. If you look forward to updating to expense tracker daily. You may find the 3-account system too simple for your taste.

It is intentionally light on tracking. People who get satisfaction from detailed spending data often prefer apps like YNAB or a zero-based budget that delivers category-level insight. The 3-account system trades that detail for simplicity and automation.

You prefer manual control over every financial decision

The 3-account system is built on automation. Transfers happen on a schedule. Accounts have set jobs. If you prefer to manually review and move every dollar each month rather than letting a structure run on your behalf, the hands-off nature of this system may feel like a loss of control rather than a relief. Some people need to be actively involved in every financial decision to feel secure and that is a valid way to manage money. This just is not the system designed for that style.

What makes this system work

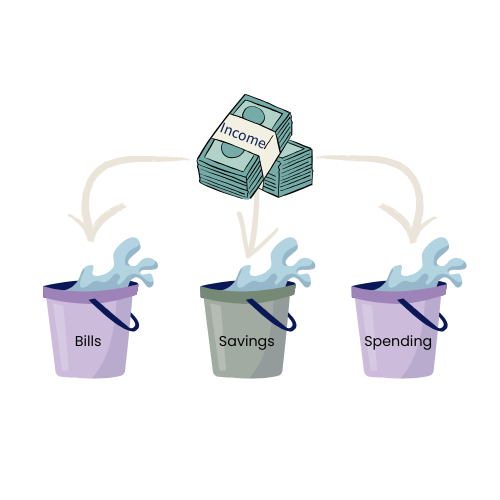

The magic isn’t in the math. It’s in the separation. When your money is structured into three accounts:

bills stop competing with spending

savings stops getting accidentally used

spending becomes guilt-free

This is the foundation introduced in the free Starter Kit — clarity first, then structure.

Signs a 3-Account Budget Is Right for You Right Now

You are a strong candidate for this system if any of the following describe your current situation:

Your money disappears too fast

You are not saving consistently or at all

You have tried other budget systems without lasting results

You feel anxious when you check your bank account

You know roughly what you earn but cannot explain where it goes

You want a financial system that does not depend on your daily attention to work

If three or more of these feel true, the 3-account system is likely the structure that has been missing from your financial life.

Is a 3-Account Budget Good for Beginners?

Yes. The 3-account budget system is one of the most beginner-friendly budgeting methods available because it is simple to understand and does not require financial experience to set up.

The core concept is something anyone can grasp immediately. The setup process requires basic math and access to a bank, nothing more.

The Breakthrough Flow™ makes the beginner entry point even lower by providing step-by-step guidance through every decision in the setup process, including exact formulas for calculating each account amount.

Can You Use a 3-Account Budget on a Low Income?

Yes. A 3-account budget system works at any income level. The system is built around your actual numbers, not a minimum dollar amount.

In fact, people on tighter incomes often benefit most from the structure. When there is less room for financial error, having a clear separation between bill money, spending money, and savings money prevents the kind of overdrafts and shortfalls that make a difficult financial situation worse.

The key is an honest setup. Calculating real account amounts based on real income and real expenses, not optimistic projections.

Can Couples Use a 3-Account Budget?

Yes. Couples can use a 3-account budget system, though the setup requires agreement on shared account amounts and individual spending allocations.

One common approach for couples is to maintain shared Bills and Savings accounts while each partner keeps a separate Spending Account. This preserves the clarity of the system while giving each person autonomy over their daily spending.

The Breakthrough Flow™ is primarily designed to work for individual or shared finances.

Ready to Find Out If This System Is Right for You?

The Breakthrough Flow™ walks you through the complete 3-account setup, with exact calculations, short video lessons, and a method built to last beyond the first month.

Comments